Consumer Lending in Nigeria

Prior to the introduction of currency, individuals in the past relied on food to settle their debts. With a promise of a crop in the spring, they would borrow seeds and distribute their crops to pay off their debts. The term consumer lending is used to describe the practice of lending money, usually in the form of a loan or credit, to individuals for personal use, purchase, or investment. The concept of credit is not new, however, the demand for it for households has grown with the rise of urbanization, the mass production of consumer products, and the gradual development of the middle class. Despite any worries around growth-trends, many would agree that the availability of consumer credit in the modern economy offers several significant economic advantages.

One of the primary advantages of consumer credit is that it facilitates the initiation of household investment undertakings in a more timely and convenient manner for many households. In this regard, household investments on credit does not mean financial investments in assets such as stocks, bonds, or mutual funds, rather, it refers to expenditure on high-value items (e.g., cars, appliances, home improvements and furnishings, educational expenses, and other leisure expenses such as boats, travels, or motorcycles) that provide long-term benefits and whose cash purchases don’t typically fit comfortably into a household’s monthly budget. By making it easier to spend on these types of investments, credit allows consumers to shift the timing of savings and consumption flows into a preferred pattern. In other words, rather than waiting until funds are available from savings (which can be a challenge for many families, particularly those in their prime earning years), one can use credit to buy the investment goods first and then pay for them as you use them; you can save for it by making payments while you’re actually using them. In exchange for this change in timing, lenders charge a fee called interest or finance charge. This charge provides a return to consumers making available the current resources. Another economic advantage of consumer credit lies in its significant contribution to the expansion of the durable goods industry, where the advent of new technologies, large-scale manufacturing, and economies have historically generated employment and wealth. Indeed, it is difficult to envision the growth of these industries without the simultaneous expansion of consumer credit to facilitate the sale of output. Easy access to credit can boost consumer spending, even during economic downturns. This can help stabilize the economy and prevent prolonged recessions.

Consumer Lending Classification

Repayment plan & Design

Consumer lending is a broad and multifaceted field that plays an important role in helping people reach their financial goals while helping the economy grow. There are many differences in consumer lending classification, such as the flexibility of the repayment plan, design of lending, types of lending, and types of lenders. Based on repayment plans, there are three basic types of consumer lending. They include non-instalment, revolving, and open-end lending plans. Non-installation is when lenders give credit in different ways but expect a single lump sum to be repaid. In revolving plan, credit is usually paid once and then paid back in a series of smaller payments, sometimes called “instalments,” usually monthly (like auto loans). Open-end is when credit is extended in different amounts and then repaid at the consumer’s preferred pace via variable monthly instalment payments within contractual limits (for example, credit card credit). Based on designs, consumer lending can either be secured or unsecured. A secured consumer loan is one that is secured by collateral if the borrower does not repay the loan. In contrast, an unsecured consumer loan is an unsecured loan that is not secured by collateral. This leaves the lender with no recourse if the borrower fails to repay the loan.

Types of Lending

Consumer loans are a wide range of financial products and services, ranging from personal loans to credit cards to auto loans to mortgage loans, and to student loans. Each type of consumer loan has its own set of uses and forms. For instance, a personal loan is one that can be used for a variety of purposes, including debt reduction, home renovation, medical costs, or holidays. Generally, the interest rate and terms of the loan are fixed. Secured and unsecured personal loans are an attractive option for people with credit card debt, who want to reduce their interest rates. Another loan type, auto loans, are secured loans tied to a vehicle. The vehicle serves as collateral, allowing borrowers to secure lower interest rates. These loans can be provided by banks, credit unions, online lenders, or car dealerships, although, loans from car dealerships tend to have higher interest rates.

Mortgage loans, on the other hand, are loans used for the purchase or refinance of residential properties. These loans typically have fixed or variable interest rates and lengthy repayment terms. Mortgage loans are typically tied to residential properties, meaning that an owner may be subject to foreclosure if they fail to make repayments on time. Mortgage loans have some of the lowest interest rates among all loans, as they are classified as secured loans. Student loans, which are also a subset of consumer loans, are loans offered to college graduates and their families to cover the cost of college education. These loans typically come in two forms: federally funded student loans and privately funded student loans. Generally, federally funded loans offer lower interest rates (due to federal subsidization of education) and more flexible repayment terms. Other types of consumer loans include Credit Cards, which are revolving credit accounts allowing consumers to make purchases within a predetermined credit limit. Generally, credit cards have variable interest rates.

Types of Lenders

Another way to classify consumer credit is by the type of institution offering the credit. Thousands of different entities have offered consumer credit over the years each serving consumers with different financial needs and purposes. Major participants include commercial bank, finance companies,

Commercial Banks

Banks are financial institutions that obtain necessary banking licenses from financial governing authorities in a country. Many banks offer a wide range of financial services to their customers including deposit accounts, as well as making deposited funds available for various types of lending to individuals, corporations, government entities, and governmental bodies. Before the development of credit cards, consumer credit lending by the depositories largely consisted of these two forms. The first is when the customer goes directly to the bank for the loan. The second is when the consumer is in fact the customer of a retailer or dealer in consumer products or services that sells the credit account directly to the bank. Today, the biggest chunk of consumer credit comes from the banking system. Credit card accounts are the most popular way to offer consumer credit. Credit cards serve as plastic identification devices that indicate the existence of a predetermined amount of open-ended credit. As mentioned earlier, consumers can draw on this credit whenever they want at the sellers of their choice.

Finance Companies

Finance companies have long been next in importance to the depository institutions (commercial banks) in providing consumer credit, and, like banks, they also are involved in a variety of areas of consumer finance. There are several smaller finance companies that are active in one or more consumer credit market segments. Some are focused on small unsecured consumer loans, while others focus on indirect financing via a network of car, home appliances, furniture, mobile homes, or other dealers. Others specialize in mortgage credit, while others issue credit cards or are involved in all of these. Regardless of the segment, the finance company industry is characterized by a wide range of sizes, products, and personalized operating methods. Additionally, there are two other types of nonbank lending company: mortgage banks, and mortgage brokers. A mortgage bank is a company that makes mortgage loans using either its own funds or borrowed funds. A mortgage broker isn’t a financial institution, but rather a matchmaker that connects mortgage borrowers with mortgage lenders. A mortgage broker typically works with multiple mortgage lenders and shops from among them to find the right mortgage for a borrower.

Other institutions

The remaining consumer creditors can be categorized under nonfinancial institutions. Nonfinancial businesses refer to consumer creditors such as retail stores that are not primarily financial institutions by assets or operations. An example are the Peer-to-Peer (P2P) Lenders, such as the cooperatives groups. These P2P lenders connect individual investors or lenders with borrowers, and facilitate loans for various purposes, often at competitive interest rates.

Lending Requirements to Know

To access lending services, consumers should the following basic information. Firstly, an applicant’s credit score is one of the most important factors a lender considers when evaluating a loan application. Credit scores have various ranges, however, are based on factors like payment history, amount of outstanding debt and length of credit history. Many lenders mostly require applicants to have minimum scores to access lending services. Lenders also impose income requirements on borrowers to ensure they have the means to repay a new loan. Minimum income requirements vary by lender and evidence of income may include recent tax returns, monthly bank statements, or signed letters from employers. If one is applying for a secured personal loan, a lender may require for pledge valuable assets—or collateral. In the case of loans for homes or vehicles, the collateral is typically related to the purpose of the loan. However, secured personal loans can also be collateralized by other valuable assets, including cash accounts, investment accounts, real estate, and collectibles like precious metals. It is important to note that in this instance, if one falls behind on payments or default on loans, a lender can repossess the collateral to recoup the remaining loan balance. Another important requirement is the request of documents to confirm identity, residence, employment, and other social economic data. Most common documents lenders require as part of the personal loan application process include proof of identity, employer and income verification, proof of address, and loan application. Having the above information beforehand prepares an applicant better to accessing various lending products and services.

Consumer Lending in Nigeria

Nigeria, the most populous Sub-Saharan African nation, has a population of approximately 214 million, according to the World Bank. Despite this, poverty remains prevalent, with a reported 65% of the population living on less than $1 per day. Income inequality is increasing, leading to unequal access to resources and amenities. The high rate of unemployment further exacerbates personal income disparities. Consumer credit facilities are thus needed to cushion the effects of this inequalities. The facility therefore becomes necessary when an individual is unable to make immediate payments for goods and services, either for their own use or for the benefit of their family.

In Nigeria, the earliest forms of credit were loans in the form of goods to the poor. However, with the development of technology and the urbanization of the country, the forms of credit changed. As consumer credit developed and became widespread, so did the attitude towards consumer credit and its role in the overall credit system. Today, consumer credit is no longer seen as a system of aid for the poor. Instead, it is widely seen as a way to meet short – term needs quickly and effectively. In a more commercial context, when banking began in Nigeria around 1892, there was no need for consumer credit products to be developed because there were few banks operating at that time. Deregulating the financial sector allowed for the establishment and licensing of many new micro-financing and merchant banks, which in turn led to aggressive competition between the commercial banks. This eventually led to the development of consumer credit products within Nigerian commercial banks. Today, the Nigerian market is saturated with various participants offering different forms of consumer lending packages.

In 2019, Consumer lending in the country totalled N1.11 trillion. Although covid 19 impacted the lending market, there was a recorded upward trend in consumer loans by 2021 as the total market share increased by 37 per cent. This expansion can be said to have been compelled through the nations apex bank (CBN). Through its loan-to-deposit ratio (LDR) policy and other improved structures to lending, the bank was able to drive financial institutions unto expanding their consumer lending products and services.

Digital Lending

Many lending platforms are taking over the consumer lending industry in Nigeria. Unlike traditional banks, which offer loans with high-interest rates, lengthy paperwork or regulations, and the requirement of guarantors, among other things, fintech businesses, are competing by offering loans that are quick efficiently. Finance, in forms of credit, has become an inseparable aspect of the global economy and is in fact critical for growth and overall prosperity. No matter how advanced an economy is, it cannot effectively develop in the absence of credit. Consumers, purchasers, and business ventures alike are highly dependent on credit in this present-day. Financial sectors, through the nature of their activities, manifests trust towards individuals and businesses by granting them credits. When credit grows, consumers can borrow and spend more, and enterprises can borrow and invest more. A rise of consumption and investments creates jobs and leads to a growth of both income and profit. This expansion of credit also influences the price of assets, thereby increasing their net worth. The rise of asset prices offers the owner the chance to borrow more, due to the increase of wealth. This cycle of credit expansion leads to increased costs, investments, creation of new jobs, prosperity, and followed by a new loan, which produces the sensation of increased wealth and make people more satisfied.

Digitization of the lending process brings several powerful benefits for financial institutions, including better decisions, improved customer experience, and significant cost savings. As consumers increasingly turn to alternative digital methods to manage their finances, the need for innovative digital products is becoming increasingly necessary to meet customers’ needs. The lending application is an innovative product created to be the most preferred solution for the processing and repayment of loans. It aims to bridge the gaps in lending processes to produce a smarter and more seamless lending experience. Lending applications have had a disruptive effect on traditional mediums by opening services, such as digital credit, to people, irrespective of their socio-economic environment. Lending Platforms, through digital credit, so far, has caused the reduction of transaction costs, possibilities for instant loan approval and disbursement, and inclusion of some part of the excluded customer base. Digital lending platforms have become disruptive technologies and they have witnessed an increased use in these recent years. Statistics have shown that the global financial-technology market is estimated to grow at a compound annual growth rate of around 20% over the next four years and is expected to reach around $5tn by 2027. In Nigeria, fintech revenue reached $543.3million in 2022, a growth from $153.1million in 2017. As consumers increasingly turn to alternative digital methods to manage their finances, the need for innovative digital products is becoming increasingly necessary to meet customers’ needs. Common digital lenders in Nigeria include Palmcredit, Carbon, FairMoney, QuickCheck, and Specta, amongst others.

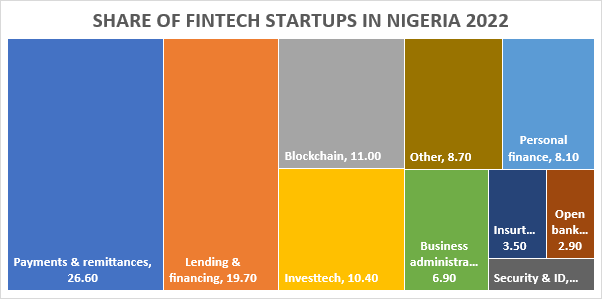

Share of fintech startups in Nigeria as of 2022, by sub-sector

As of 2022, most fintech startups in Nigeria specialized in payments and remittances. This referred to nearly 27 percent of 173 ventures. Moreover, fintech ventures in lending and financing represented a share of over 19 percent, while those operating in blockchain accounted for 11 percent of the total.

Consumer Lending Challenges

Even though consumer credit is important for consumers and the economy, increasing consumer debt over time continues to pose challenges for lenders. The high default rate is a major concern for lenders. In Nigeria, the consumer credit system is relatively under-developed, and lenders have limited access to the credit history data of borrowers. This makes it difficult for them to make accurate and timely lending decisions and effectively manage risk. As a result, lenders tend to be conservative in their lending practices and charge higher interest rates for the risk they are taking on. Regulation is essential to protect consumers, lenders, and financial stability, but an over-restrictive regulatory environment can impede innovation and credit access. For example, if the Central Bank of Nigeria (CBN) decides to raise the LDR of the commercial banks, the interest rates will increase, which will discourage consumers from taking on loans. Regulators in Nigeria face the challenge of balancing consumer protection with industry growth. In addition to these stringent regulations are archaic and obsolete laws that do not fit into modern day financial transactions.

A robust consumer credit system and banking system would have a positive impact on financial intermediation, as it increases the ability to mobilize and distribute savings to key areas of Nigeria’s economy. However, due to a lack of data, banks are unable to make lending decisions, thus excluding millions of potential borrowers. This lack of information, combined with a lack of access to financial infrastructure and digital technology, may limit the range of consumer lending options available. However, as digital lending platforms become increasingly popular, cyber security and fraud have become major issues. Fraudulent loan requests and data breaches can result in financial losses for lenders and borrowers alike. Furthermore, as more lenders become involved in the consumer lending sector, competition increases. This can result in predatory lending practices, which can be detrimental to both borrowers and lenders.

Debt recovery in Nigeria can be a time-consuming and expensive process due to the complexity of the legal system and the backlog of cases. Inefficiencies in legal procedures and a lack of evidence to support government policies and guidelines can discourage lenders from pursuing borrowers who have defaulted, thus reducing their profitability. In addition to these legal restrictions in debt recovery are cultural obstacles. Apart from its crucial role in debt recovery processes, Cultural barriers also play an important role in preventing women from accessing credit. Many women are denied access to credit because of socio-economic factors, such as family history, tribe & ethnic origin, religious belief, etc.

There is also the issue of what happens if the consumer credit market goes wrong for the consumer to the point where the consumer is unable to repay the loan on time or even at all. Nigeria’s economy is prone to fluctuations due to the fluctuation of oil prices, insecurity, and political instability, among others. Economic uncertainty increases the chances of loan defaults and affects the stability of consumer lending market. In addition to economic and legal factors, environmental factors can also affect an individual’s ability to repay loans significantly. For example, the covid 19 pandemic had a huge impact on consumer lending activities in Nigeria. Many people were unemployed and had reduced disposable income, which reduced their ability to repay.

To overcome these difficulties, a variety of stakeholders, including government, regulatory bodies, financial institutions and FinTech companies, must work together to foster a more enabling environment for consumer credit. This could include improving credit reporting processes, strengthening regulatory frameworks, increasing financial literacy, and promoting responsible lending practices to ensure long-term growth in the industry while safeguarding consumers.

Action

The proliferation of digital technologies has been a significant factor in the widespread acceptance of consumer credit. Today’s consumers can access various financial services and products through digital platforms and mobile applications. Using digital lending platforms has allowed creditworthiness assessments to be conducted quickly and loans be disbursed cost-effectively. This process has simplified obtaining loans and credit and provided lenders new opportunities to reach a broader range of customers. By encouraging fintech innovations in consumer lending, it is possible to increase the accessibility and affordability of credit. Also, to ensure the success of sustainable lending initiatives, there is a need for efficient collaboration between governments, financial institutions, financial authorities, and regulatory bodies. This collaboration will prevent harmful lending procedures and help to ensure that credit is accessible to all. Regulators must continuously provide and enforce responsible, healthy lending guidelines to ensure financial institutions comply with ethical lending practices, such as interest rate caps and anti-predatory lending rules. To provide a healthy, competitive market, regulators must assist institutions in managing risk effectively. To achieve this, these regulators can provide subsidies, grants, or credit guarantee schemes to institutions, particularly those offering loans to disadvantaged populations, including low-income individuals; these incentives can make lending more appealing to consumers. Training and capacity-building initiatives for financial institutions, particularly fintech firms, can also improve lenders’ capacity to assess credit risk and manage loan portfolios and their ability to implement them. Establishing monitoring and reporting mechanisms for consumer lending practices can assist in identifying and addressing issues such as fraud, and over-indebtedness, as well as initiatives that promote financial literacy among consumers, such as educating individuals on responsible borrowing, saving & budgeting, and debt management. In the lending space, data privacy and security must be a priority for lenders, as data breaches and the mishandling of personal information can cause harm to consumers and eventually damage trust in their platforms.