EDUCATION INDUSTRY REPORT

“Continuous learning is the minimum requirement for success in any field.” — Brian Tracy

Over the course of thousands of years, education has changed as a result of cultural, religious, social, economic, and political influences. Ancient education was generally reserved for the elite and concentrated on teaching practical skills, religious ceremonies, and developing officers and administrators. These ancient civilizations included Mesopotamia, Egypt, Greece, and Rome. There wasn’t much formal education, and it was frequently delivered through private tutoring or apprenticeships. During the Middle Ages, the majority of educational institutions were monasteries and cathedrals. The main teachers were monks and clergy, and the main subjects studied at school were theology, philosophy, and Latin. The Renaissance era saw a resurgence of humanism (the study of human concerns); the era focused on a broader curriculum that covered the arts, sciences, and literature. At this time, the printing press significantly contributed to the dissemination of information by increasing the accessibility of books.

In the 17th and 18th centuries, public education systems began to take form; an advancement that began as a result of the emergence of modern nations. These systems attempted to train people for civic engagement and workforce requirements while also delivering basic education to a larger populace. The Industrial Revolution of the 18th and 19th centuries brought significant social and economic changes, leading to a growing need for an educated workforce. Many industries needed many educated workers and as a result, the expansion of public schooling and the introduction of compulsory education laws in many nations. Significant improvements in education occurred during the 20th century, including the creation of higher education institutions, the expansion of primary and secondary education, and the introduction of specialized vocational training. Theories of child development, progressive education, and educational psychology were all included into the philosophical and practical approaches to education as they developed. These inclusions made education more accessible to people, bringing about a renewed educational system. Globalization, technological development, and the need to meet new challenges and opportunities in a world that is ever changing also contributed to this advancement. Today, online learning and educational technology have become increasingly popular due to the revolutionary changes brought about by computers, the internet, and educational software. The history of education reflects humanity’s ongoing quest for knowledge and development, and also shows its importance in the development of economies, and more especially in creating sustainable wealth and growth. As such, education remains a key requirement in global advancement.

Education, in its broadest general sense, is the means by which society transmits its accumulated skills, customs, and values from one generation to another, and is provided in three different ways which are the formal, non-formal, and the informal process. As a formal process, schooling has become an important mode of education. Formal education is a planned and structured type of education, and through schooling, carefully planned and well-structured instructions through the use of syllabuses, scheme of work, and course outline are taught to students. The Non-formal education is different from the formal education as that what is learned is structured but not as strict as that of formal education, more so there is more flexibility to the venue, methods of learning and the instructor. The non-formal education is purposively meant to meet specific learning needs of particular groups of children, youths or adults in the community. It includes various types of vocational, educational and socio-personal activities such as remedial training, skill training, apprenticeship to vocational work like tailoring, hair-dressing, tie and dye, barbering, automobile engineering, painting, carpentry, and amongst others. The informal education involves a type of education that comes naturally, it is neither planned nor structured. In this form, there are no specific instructors, supervision is not required, and most of the learning is unconscious and involuntary. An example of this mode of education is the various learning a child experiences from family, religious affiliation, peer groups, friends, association’s experience, mass media, and the environment.

Value Chain

The Education sector comprises establishments whose primary objective is to provide education. These establishments can be public, non-profit, or for-profit institutions. They include elementary schools, secondary schools, community colleges, universities, and ministries or departments of education. The entire process and sequence of activities involved in delivering educational products and services to learners is referred to as the education value chain. It encompasses the various stages and actors involved in providing education, from authors/content developers to student learning outcomes. Understanding the education value chain is crucial for analyzing and optimizing the efficiency and effectiveness of educational systems. It enables stakeholders, including as legislators, educators, and administrators, to pinpoint problem areas, improve learning results, and guarantee that educational institutions are in line with the requirements of both students and society at large. It also aids in addressing issues like equity, accessibility, and educational quality.

The educational value chain can be broadly divided into four elements; the mapping competence action, the competence modules action, the training action, and then the profits (which we can refer to as the outcome in the labor market). Like an upstream to downstream movement, the value chain starts from recognizing competence needs, creating contents to develop those needs, the actual training, and then the outcome of the process. With research and curriculum development and content creation from authors, research to identify learning needs, trends, curriculum development, and the development of educational materials, textbooks, digital resources, and multimedia content are initiated. In this chain process, teachers and instructors are trained to enhance their teaching skills and subject knowledge. Proper training and professional development programs ensure that teachers are equipped with the necessary knowledge and teaching methodologies to deliver quality education. Also, educational institutions are vetted to ensure they meet quality standards and accreditation requirements.

At the next stage – the training phase, teachers and educators deliver the educational content and facilitate the learning process in classrooms or online environments. They engage with students, provide explanations, and conduct assessments to evaluate learning progress. Assessment methods, such as tests, exams, and assignments, are used to measure students’ understanding and progress. This data is then used to evaluate the effectiveness of the teaching methods and the curriculum itself. Today, other sub processes are being included in the education value chain to ensure efficiency and effectiveness of outcomes. There are now provisions of counseling, academic guidance, and support for students’ personal development, and special education and resources for students with specific needs. Improved technological know-how has now called for the implementation and maintenance of technology infrastructure to support teaching and learning. And parents and guardians are now encouraged to involve more in their ward’s education. The last phase, which is the profit/outcome, is the stage where students are issued diplomas, degrees, or certifications upon successful completion of programs. Also in this phase, feedback from students, teachers, and stakeholders are collected for continuous improvement. Today, lifelong services are encouraged. Beyond formal education, lifelong learning initiatives offer opportunities for individuals to continue acquiring new knowledge and skills throughout their lives.

Segments of the Education Industry

The education industry is grouped into three segments: the consumers, institutions, and the workers. Although all segments of the industry are wholly customers, “primary customers” who receive the services directly, “secondary customers” who directly influence the education for specific individuals and institutions, like families and employers, and “tertiary customer” who has a minor but very important role in education, like employers, government employees, and society as a whole, the primary customer is the student. Students can be thought of as the consumers of the education industry. They need the support of dedicated educators to achieve their educational goals and obtain the knowledge and skills they need. All other industries can be considered as consumers of the education industry for they depend on it skilled labor.

The second segment, the institutions, include the various public and private schools, colleges, and universities. Vocational education centers also provide job-oriented education through the apprenticeship. Other institutions include ancillary education services such as charter schools, special schools, and educational content suppliers. The institution performs by utilizing information such as financial and student data to plan, evaluate, and implement strategies that can improve student’s learning outcomes. While the last segment, the workers, include administrators, teachers, librarians, lecturers, professors, sports coaches, counselors, etc. Textbook publishers and assessment providers also play important roles in this segment. All workers in this industry are tasked with helping students achieve all their educational goals. These three segments interconnect to boost the education industry, they make efficient use of available resources to improve enrolment numbers, student learning outcomes, and overall operational efficiency.

The educational industry contributes majorly to the global economy. It is tasked with the development of advanced minds and the provision of the talent pool for other industries, thus, its strong emphasis. This analysis examines the processes in the education industry, and how it performs globally and in Nigeria in terms of education output. The report also provides data for production, market size, industry’s costs, industry’s profitability, and other number of insights.

Global Analysis

Education today had evolved; it is not only perceived as a right, but also as a duty – governments are expected to ensure access to basic education, while citizens are then required by law to attain education up to a certain basic level. History shows that throughout the last two centuries, education has grown significantly around the world. This is evident in all quantity measurements. Over the past two centuries, there has been an increase in the number of people around the world who are literate, mostly due to rising primary school enrolment rates. The average number of years spent in secondary and tertiary education has increased dramatically and is today far more than it was a century ago.

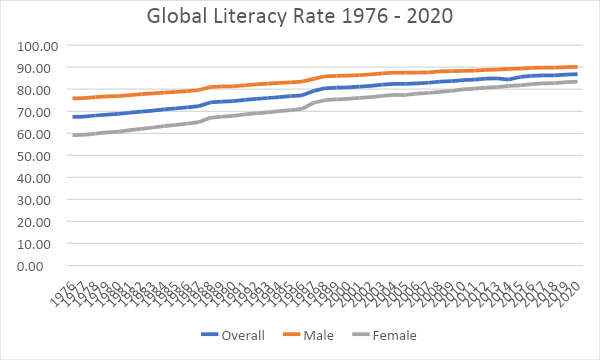

Global adult literacy rate aged 15 years and older from 1976 to 2020.

Statista

In the past five decades, the global literacy rate among adults has grown from 67 percent in 1976 to 86.8 percent in 2020.

Analysis by Segment

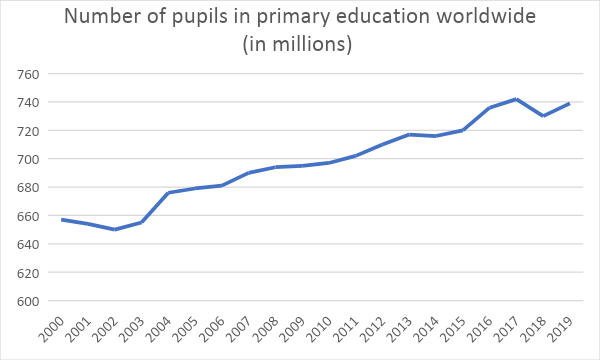

Primary

Statista

The number of pupils in primary education worldwide increased over the past many years. While around 657 million children were enrolled in primary school in 2000, the number reached about 739 million pupils in 2019. The highest number of pupils, however, were registered in 2017, peaking at 742 million. During the same time period, more and more pupils completed primary education, standing at nearly 90 percent in 2019. However, the highest share of children out of primary school was in Sub-Saharan Africa, where 22 percent of girls and 17 percent of boys were not in school in that year. A higher proportion of girls than boys were also out of lower secondary school, reaching 16 percent worldwide as of 2018.

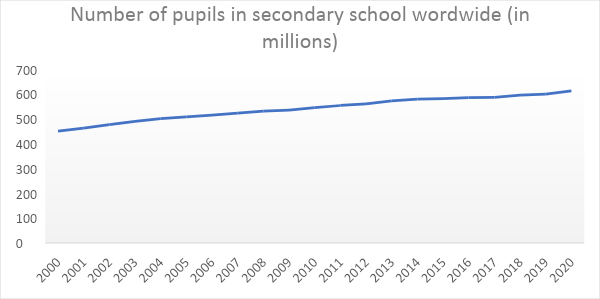

Secondary

Statista

The number of students in secondary education also increased significantly. About 452 million children were enrolled in some kind of secondary education in 2000; a number which has grown to 601 million in 2019. At the same time, the completion rate of lower secondary education also increased, reaching over 76 percent that same year.

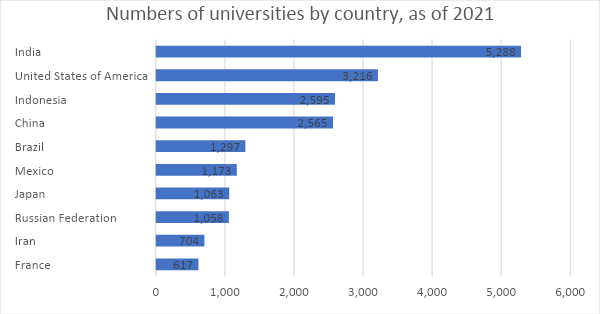

University

Statista

There are over 15 thousand universities in the world. Based on the above data, India has the most universities worldwide. According to 2021 data, there were an estimated 5,288 universities in India. The United States had the second most universities counting 3,216, followed by Indonesia with 2,595 universities. Nigeria is number 26, with about 279 universities.

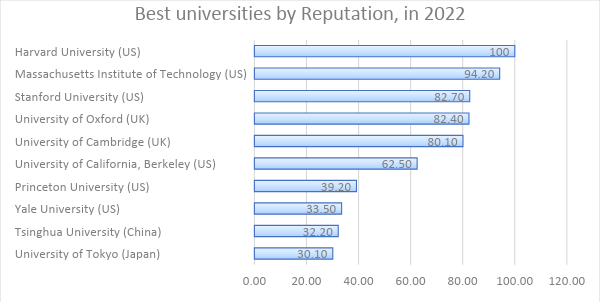

Statista

In 2021, Harvard University was placed first as the university with the highest reputation score worldwide at 100. Second on the Times Higher Education world university ranking was Massachusetts Institute of Technology (MIT) with a reputation score of 94.2, followed by the Stanford University. A high number of the leading universities in the world are located in the United States and the United Kingdom. Other universities such as Tsinghua University in China, University of Tokyo in Japan, and ETH Zürich in Switzerland, are ranking next.

Public vs Private Education

Developing countries have been urged to diversify their sources of educational finance since the early 1980s. Claims of the greater efficiency of private schools have been advanced as part of the argument supporting such advice, though the main thrust has been the financial stringency of central government. Both types of education systems play crucial roles in the overall education landscape, and the choice taken depends on various factors and priorities. For instance, the advantages of going for a public education will amongst others include the easy access to education. Public education is generally more accessible to a broader range of students, regardless of their socio-economic background. This type of education system can help promote equal opportunities and reduce educational disparities. Public schools are funded and operated by the government. They receive funding from taxpayers, and in some cases, there may be additional grants or support from the central or local government. This constant cash inflow provides the security for more facilities and equipment needed by students and instructors. However, issues concerning quality of curriculum content, instructors, and equipment other times discourages the pursuit of public education.

It is important to note that the definition, in this context, of a public education is the type of education process controlled and funded by the government, while that of the private system by private stakeholders. As with the private education form, the diversity of options, innovation and flexibility, additional and increased funding, and advanced resources makes it a supposed better option, in some countries. In many cases, it is not a matter of choosing one over the other, but rather striking a balance and ensuring a well-rounded education system. Governments may choose to invest in public education to uphold their responsibility to provide accessible and quality education to all citizens. At the same time, private education can complement the public system by offering alternative educational approaches and encouraging healthy competition. Ultimately, both systems play crucial roles in shaping individuals and societies, and a holistic approach to education is often the most beneficial. Governments can focus on improving public education to enhance accessibility and quality while also supporting policies that foster a diverse and thriving private education sector.

Expenditure

For a number of early-industrialized countries, educational expansion took place mainly through public funding. Today, public resources still dominate funding for the primary, secondary and post-secondary non-tertiary education levels in these countries. Although private schools educate, in most countries, only a small proportion of children, there is widespread interest in their process that is different from public schools, and in what their effect might be on other schools, on the education system as a whole, and on society.

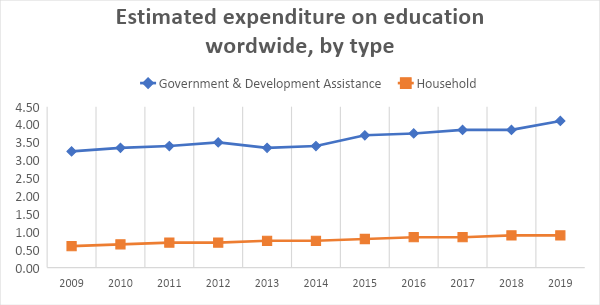

Estimated government, household, and official assistance spending on education worldwide from 2009 to 2019 (in trillion U.S. dollars)

Statista

In 2019, global education expenditure amounted to approximately five trillion U.S. dollars, with the vast majority of this spending being from governments, or from development assistance. Private households spent around 900 billion dollars in 2019.

More than three quarters (76%) of global education spending stems from government, and households contributed a little less than one-quarter in 2020. But in low-income countries that share was 35%. In comparison, households in high-income countries contributed 16% of total education spending. One in three countries spend less than 4% of their GDP and less than 15% of their budget on education. In low- and middle-income countries, spending on education rose by 5.9% a year between 2009 and 2019. Between 2010–11 and 2018–19 government education spending as a percentage of GDP remained at 4.3% in lower-middle-income countries and increased from 3.2 to 3.5% in low-income countries. Three-fifths of education resources in low-income and lower middle-income countries come from domestic public expenditure, primarily supplemented by private household expenditures. About 40% of low- and lower-middle-income countries spend below international benchmarks for public education spending. These countries continue to bear a significant portion of education costs, accounting for 39% of the total spending in education compared to 16% in high-income countries. Education spending in these countries would need to increase from 3.5% to 6.3% of GDP between 2012 and 2030 to deliver universal pre-primary, primary and secondary education. In sub-Saharan Africa, households account for 38% of total education spending, ranging from less than 5% in Ethiopia, Lesotho and Sao Tome and Principe to more than 67% in Ghana, Liberia, and Nigeria.

Global market share

The global educational services market grew from $3,173.75 billion in 2022 to $3,421.26 billion in 2023 at a compound annual growth rate (CAGR) of 7.8%. The educational services market is expected to reach at least $10 trillion by 2030 as population growth in developing markets fuels a massive expansion and technology drives unprecedented re-skilling and up-skilling in developed economies. The next decade will see an additional 350 million post-secondary graduates and nearly 800 million more primary graduates than today. In the global Educational Services segment, USA, Canada, Japan, China, and Europe will drive the CAGR estimated for this segment. The Educational Services market in the U.S. was estimated at US$353.2 Billion in the year 2020. The country currently accounts for a 28.89% share in the global market. China, the world second largest economy, is forecast to reach an estimated market size of US$361.5 Billion in the year 2027 trailing a CAGR of 10.3% through 2027. Among the other noteworthy geographic markets are Japan and Canada, each forecast to grow at 3.7% and 6.1% respectively over the 2020-2027 period. Within Europe, Germany is forecast to grow at approximately 4.3% CAGR while the rest of European market will reach US$361.5 Billion by the year 2027.

These regional markets accounting for a combined market size of US$55 Billion in the year 2020 will reach a projected size of US$79 Billion by the close of the 2027. China will remain among the fastest growing in this cluster of regional markets. Led by countries such as Australia, India, and South Korea. The market in Asia-Pacific is forecast to reach US$266.7 billion by the year 2027, while Latin America will expand at a 7% CAGR through 2027. Top competitors identified in this industry market include Cisco Systems, Inc., Columbia University, Harvard university, and Microsoft Corp, among others. The leading educational services regions include North America (United States and Canada), Europe (Germany, UK, and France), Asia-Pacific (China, Japan, and Korea), South America (Brazil, Argentina, Columbia), and Middle East and Africa (Saudi Arabia, UAE, Egypt, Nigeria, and South Africa).

Covid-Impact

COVID-19 wreaked havoc on the education industry worldwide. The disruption of societies and economies caused by the pandemic aggravated the already existing global education crisis and impacted education in unprecedented ways. Globally, between February 2020 and February 2022, education systems were fully closed for in-person learning for 141 days on average. In South Asia and Latin America & the Caribbean, closures lasted 273 and 225 days, respectively. Even before the COVID-19 pandemic, this global learning crisis was stark. The learning poverty indicator, created by the World Bank and UNESCO Institute of Statistics and launched in 2019, gives a measure of the magnitude of this learning crisis: In low- and middle-income countries, the share of children living in learning Poverty – already 57% before the pandemic – reached 70% given the long school closures and the wide digital divide that hindered the effectiveness of remote learning during school closures, putting the SDG 4 targets in jeopardy. One billion children saw their in-person education interrupted for more than a year. For many, the interruption was for 2 years. Children and youth in most countries suffered major learning losses during the pandemic. Rigorous empirical evidence from various countries, including low-, middle-, and high-income contexts across regions, reveals very steep losses. School closures and ineffective remote learning caused students to miss out on learning and to also forget what they had learned: on average, for every 30 days of school closures, students lost about 32 days of learning.

COVID-19 created an inequality catastrophe. Almost all countries provided some form of remote education during school closures, but there was high inequality in access and uptake between and within countries. Children from disadvantaged households were less likely to benefit from remote learning than their peers, often due to a lack of electricity, connectivity, devices, and caregiver support. Girls, students with disabilities, and the youngest children also faced significant barriers to engaging in remote learning. Overall, at least a third of the world’s schoolchildren – 463 million globally – were unable to access remote learning during school closures. In addition to these challenges is the negative impact of the unprecedented global economic contraction on family incomes, which increases the risk of school dropouts, and results in the contraction of government budgets and strains on public education spending. Youth have also suffered a loss in human capital in terms of both skills and jobs. In many countries, these declines in youth employment were more than twice as large as the declines in adult employment. As a result, this generation of students, and especially the more disadvantaged, may never achieve their full education and earnings potential.

Globally 40% of countries trained three quarters or more of teachers on distance learning methods including various forms of ICT in 2020, ranging from 65% of countries in Latin America and the Caribbean to just 8% in sub-Saharan Africa during the pandemic. 41% of lower income countries reduced their spending on education after the onset of the COVID-19 pandemic in 2020, with an average decline in spending of 13.5%. it was estimated that the global learning losses from COVID-19 could cost generation of students close to US$21 trillion in lifetime earnings, which far exceeds the original estimate of US$10 trillion made immediately after the pandemic outbreak and even the US$17 trillion estimated in 2021.

The Russia-Ukraine war disrupted the chances of global economic recovery from the COVID-19 pandemic, at least in the short term. The war between these two countries has led to economic sanctions on multiple countries, surge in commodity prices, and supply chain disruptions, and affecting many markets across the globe.

EdTech

Due to the COVID-19 pandemic, many schools across the world were forced to close, which left more and more grade-school students participating in online learning, and university-level students enrolling in online courses to enforce distance learning. Organizations such as UNESCO enlisted educational technology solutions to help schools facilitate distance education. The pandemic’s extended lockdowns and focus on distance learning has attracted record-breaking amounts of venture capital to the ed-tech sector. In 2020, in the United States alone, ed-tech startups raised $1.78 billion in venture capital spanning 265 deals, compared to $1.32 billion in 2019. A popular segment of the EdTech market is the education apps market. The education apps market is estimated to grow at a CAGR of 28.61% between 2022 and 2027. The size of the market is forecast to increase by USD 124,782.56 million. The growth of the market depends on several factors, including growing government initiatives, growing demand for STEM-based apps and an increase in penetration of cellular internet.

Growing government initiatives are key factors driving the global education application market growth. Governments of developing countries like India are taking several initiatives to boost the growth of the e-learning industry. For instance, in response to the COVID-19 pandemic, the Indian government has implemented a number of initiatives to bring the e-learning industry on par with some international best practices in online education and also relaxed regulations to allow universities and colleges to provide students with extended online and distance learning opportunities. Technology developments such as Augmented reality and virtual reality have resulted in the evolution of numerous learning apps, especially for students who are pursuing an education in subjects such as medical sciences and engineering, which require extensive practical learning. Further, many students have begun to show a keen interest in downloading and using activity-tracking apps embedded with learning analytics as they believe these apps play a vital role in providing data-backed information that can improve their overall learning activities. For colleges and universities, especially in developed regions, the inclusion of education apps has become a key component of their marketing strategy. Apart from enhancing learning processes, higher education institutions are using apps for activities such as developing target groups of students to promote an appropriate set of courses for them for enrolment.

Asia-Pacific is projected to contribute about 41% to the global market share by 2027. The market in Asia-Pacific is expected to witness exponential growth during the forecast period. This is attributed to the large consumer base, increasing awareness about education apps, growing Internet penetration, the adoption of smartphones, the increasing emphasis on technology by educational institutions, and favorable government initiatives. With nearly 500 million new subscribers added since 2014, Asia-Pacific is one of the fastest-growing regions in the world for mobile services and is home to over half of the total number of global subscribers.

Key EdTech Companies

Statista

Statista

Data reflects only revenue from in-app purchases.

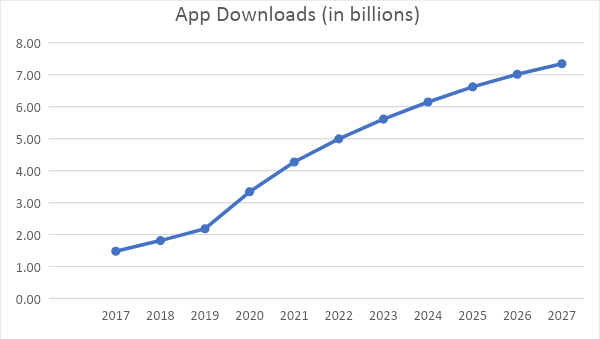

App downloads from 2017 to 2017

Statista

Continent Analysis

Literacy

Statista

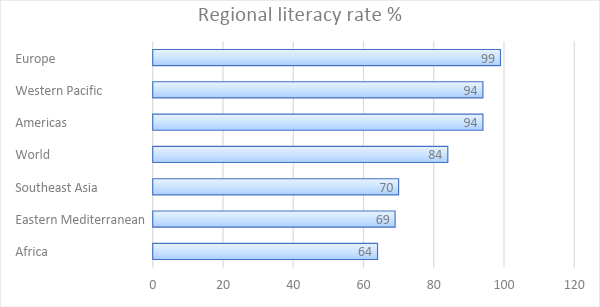

Literacy rates worldwide as of 2012, by region

From a historical perspective, the world’s population has experienced a dramatic increase in literacy rates. In 1820, just 12% of the world’s population could read and write, but today that number has reversed: only 14% of people worldwide were still illiterate in 2016. The global literacy rate rose by 4% per five years during the past 65 years, from 42% in 1960 to 86% in 2015. Despite large improvements in the expansion of basic education and the ongoing reduction of educational disparities, there are still a lot of obstacles. There are still sizable populations that lack access to basic education in the world’s poorest nations, where this is most likely to constitute a development barrier. For instance, just 36.5% of youngsters (15–24 years old) in Niger are literate. From the above data, we see these disparities in the region of Africa and the Eastern Mediterranean. Global economic and cultural disparities are the primary causes of these discrepancies. Families with low resources are frequently less likely to support their children’s education in poorer nations.

Segments

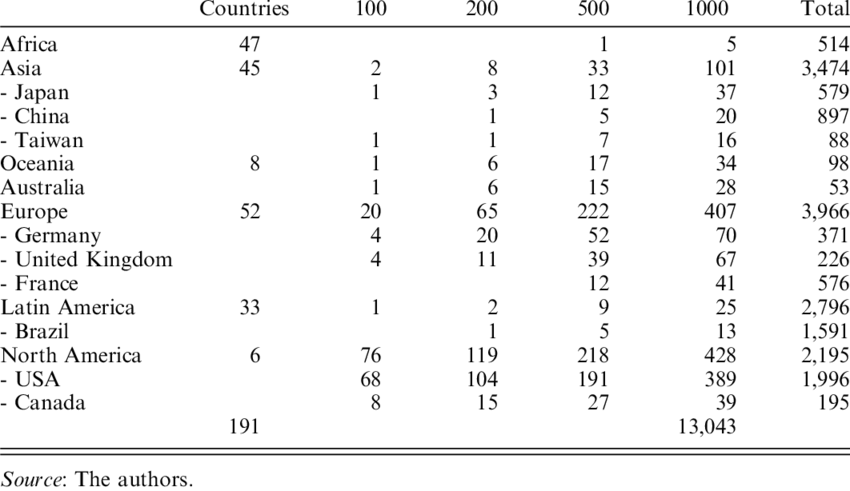

Number of universities distributed by region (with leading countries within the region) according to their presence in the top 100, 200, 500, and 1,000 institutions of the webometric ranking.

Publishing firms

As of 2023, the global book publishing industry has a market size of $114.9 billion and is projected to grow at a CAGR of 6.1% through 2027. At least 1.7 million books are published each year. North America was the largest market for books, with a global share of over 30% in 2021. The presence of a large number of independent publishers and publishing companies in the region is anticipated to boost market growth. Additionally, the growing number of avid readers in North America is likely to benefit the market. Amazon is the largest book retailer in North America, followed by Barnes & Noble. Furthermore, hardcover books are expected to hold the largest market share, while audiobooks are anticipated to witness rapid growth. The penetration of e-books is also anticipated to increase in the region. A large number of physical retail bookstores have been facing challenges, with a rising number of readers switching to online shopping or opting for subscription-based e-books. Asia Pacific is expected to witness a CAGR of 2.5% from 2022 to 2030. The Asia Pacific market for books is currently in the growth phase. The region is dominated by local publishers, and the demand for international books is anticipated to increase. However, many diverse languages are prevalent in this region, and thus, the demand for books in regional languages is higher compared to English books. Some of the key players operating in the global books market include Penguin Random House, Hachette Book Group, HarperCollins Publishers, Simon & Schuster, Inc., Pearson, Macmillan Publishers, Scholastic Inc., Marvel Comics, Morris Publishing, and IDW Publishing.

Africa

The growth in the world’s labor market is in Africa. As other parts of the world begin to age, Africa will grow its population and today’s children will be the talent tomorrow’s global companies will be recruiting. In the next 30 years, it is projected that sub-Saharan Africa’s working-age population will increase more than twofold—accounting for 68 percent of the world’s total growth. Since the early 2000s, African countries have made efforts to improve access to education. The proportion of primary school age children who are not in school has halved – from 35 per cent in 2000 to 17 per cent in 2019. The proportion of children of lower secondary school age who are not in school dropped from 43 per cent to 33 per cent in the past two decades, and for children of upper secondary school age, it dropped from 63 per cent to 53 per cent. Although Africa is still behind in the global literacy rate, counties in the continent continue to develop strategies and programs to improve education.

The Africa e-learning market size was approximately US$ 2.8 Billion in 2022. The key factors that drove the market market include the focus on improving the literacy rate, the rising sales of smartphones, and the increasing popularity of wireless communication technologies. The growing adoption of online learning solutions and platforms, coupled with the introduction of world-class educational facilities will continue to propel the market growth in the coming years. As such, the Africa E-learning market is expected to exhibit a CAGR of 11% during 2023-2028. The growing prominence of E-learning platform as an electronic network to transfer skills and knowledge with the flexibility to fit in many recipients at the same or different time schedules, is primarily driving the Africa E-learning market. On a regional level, the market has been prevalent in countries like South Africa, Morocco, Nigeria, Tunisia, and Kenya, where South Africa currently dominates the Africa E-learning market followed closely by Nigeria. Some of the major players in the Africa E-learning market include Via Afrika, Obami, Dapt.io, Eneza Education, Tutor.ng, uLearn, AltSchool, amongst others.

Asia

The Asia smart education and learning market was valued at $43.36 billion in 2020, and is projected to reach $369.34 billion by 2030, registering a CAGR of 23.6%. Adoption of smart education & learning solutions has increased over a period of time, as a number of educational institutes are shifting their preference towards smart education concept by adopting high-tech teaching methods. In the Asia, the Covid-19 pandemic has significantly led to the increased adoption of digital technologies with an augmented data traffic. The closure of schools and other learning spaces in developing nations such as India and China have primarily boosted demand for smart education and learning solutions in the region. The hardware segment dominated the Asia smart education and learning industry in 2020 and is expected to maintain its dominance in the upcoming years. Rise in adoption of interactive displays primarily drives the growth of the hardware segment in Asia smart education and learning market. Such displays are designed for any learning environment and are easy to use, deploy, and support. However, services are expected to witness highest growth rate owing to its rising demand from the end users as it ensures effective functioning of software throughout the process. On the basis of end user, the academics segment dominated the overall Asia smart education & learning market share in 2020, owing to continuous ongoing improvement in educational infrastructure and customization of learning & assessment processes, due to increase in investments in digital resources. However, corporate segment is expected to witness highest growth rate during the forecast period. China dominated the overall Asia smart education and learning market in 2020. This is mainly attributed to the rapid development of China’s education sector and its inclination toward intelligent technologies. In addition, the players in this country are actively introducing advanced smart education and learning products, further boosting growth of the market. For instance, in December 2019, Tencent Holdings Ltd., the Chinese internet giant on launched WeLearning, a new smart education solution to meet significant demand of country’s booming smart education market.

Post covid-19, the Asia smart education & learning market was valued at $43.36 billion in 2020, and is projected to reach $369.34 billion by 2030, registering a CAGR of 23.6%. The current estimation of 2030 is projected to be higher than pre-Covid-19 estimates. In the Asia, the pandemic has significantly led to the increased adoption of digital technologies with an augmented data traffic. The closure of schools and other learning spaces in developing nations such as India and China have primarily boosted the demand for smart education and learning solutions in the region. There has been greater adoption of adaptive and mixed learning approaches during the pandemic.The stay-at-home orders in Asia caused the transformation of education and learning sector toward online approach, leading to the distinctive rise of e-learning; thereby, teaching is undertaken remotely and on digital platforms. For instance, BYJU’s, a Bangalore-based educational technology company has seen a 200% increase in the number of new students using its Think and Learn app in April 2020. Hence, rapid inclination toward e-learning during the pandemic drives the growth of the Asia smart education and learning market.

Oceania

The Australian online education market stood at around $ 4 billion in 2018 and is anticipated to grow at a CAGR of over 8% to cross $ 7 billion by 2024 on account of technological advancements, eager learners and increasing penetration of smart devices. The need for user-friendly, secure, and convenient method to learn and study is rising across Australia and is fueling growth in online education market. Advancements in the field of artificial intelligence are expected to boost the growth rate of the market in the coming years, platforms that facilitate learning through gaming are gaining popularity. And improvements in IT security and implementation of cloud-based solutions have increased the adoption rate of online education system as people can enjoy a smooth learning experience on safe online platforms. The Australian online education market can be segmented based on technology type, provider, application, and region. On the basis of technology type, the market can be segregated into mobile e-learning, learning management system, podcasts, rapid e-learning, virtual classroom, and application simulation tool. The major players operating in the online education market of Australia include Mc Graw Hills Australia, Cisco, Academies Australasia Group Limited, Adobe systems, Pearson, Blackboard Australia Pty Ltd., Navitas Limited, IDP Education Proprietary Limited, etc. Major companies are developing advanced technologies and launching new products in order to stay competitive in the market. Online education providers rely on the accessibility of online material. Faster and more reliable internet connections facilitate growth in online education, especially in remote areas. Internet subscriptions are largely saturated in metropolitan regions, with new subscribers highlighting the trend towards online education access among regional Australia. The number of internet connections in Australia is expected to escalate by 2.2% in 2022-23, providing an opportunity for online providers.

The market size, measured by revenue, of the Education and Training Australian industry was $144.6bn in 2022. The Education and Training division provides education services through preschools, primary and secondary schools, technical colleges, training centers, and universities. The market size of the Education and Training industry in Australia has grown 0.8% per year on average between 2017 and 2022. Preschool, primary, and secondary education funding models are supporting revenue growth. Recurrent government spending for education provides a huge proportion of total division revenue. Changes to government funding exert a huge influence on the division. Primary and secondary school funding has climbed providing a benchmark amount per student, plus additional funding to address disadvantages for some students. The three biggest companies in the Education and Training in Australia industry include the New South Wales Department of Education (NSW), Department of Education and Training Victoria, and Queensland Department of Education and Training.

America

Latin America

The education technology market in Latin America is expected to generate revenues of over $4 billion by 2023. This transformation is due to globalization, talent migration, and improvements in corporate competencies and Government initiatives. Latin America’s e-learning market has been experiencing significant growth in recent years. According to estimates, the market size reached around $3.8 billion in 2020 and is projected to grow at a compound annual growth rate (CAGR) of approximately 8.2% from 2021 to 2026. The region has witnessed a surge in internet penetration, which has played a crucial role in driving the growth of the e-learning market. As of 2021, around 68% of the population in Latin America had internet access, and this number is expected to increase further in the coming years. Mobile devices, such as smartphones and tablets, have become increasingly popular in Latin America, enabling access to e-learning platforms on the go. It is estimated that mobile learning will account for a significant portion of the e-learning market in Latin America. E-learning platforms in Latin America are catering not only to traditional educational institutions but also to the corporate sector. Many companies are investing in e-learning solutions for employee training and professional development, driving the demand for specialized e-learning content and platforms. Governments in various Latin American countries are recognizing the importance of e-learning and investing in initiatives to promote its adoption. For example, the Brazilian government launched the National Program of Access to Technical Education and Employment (Pronatec) to provide vocational training through online platforms. Institutions are increasingly eliminating the traditional method of educating students using the textbook-and-blackboard format and are now turning toward digital platforms such as one-on-one computing to impart knowledge. The most educated Latin America countries include Brazil, Argentina, Colombia, Mexico, Peru, and Costa Rica.

North America

The Education market in North America is projected to grow by 11.58% (2022-2027). The U.S. Education Market was estimated at USD 1.4 trillion in 2021 and is anticipated to reach around USD 3.1 trillion by 2030, growing at a CAGR of roughly 4.2% between 2022 and 2030. The education sector in the U.S., after covid-19, has undergone several transformations and has turned more receptive to student needs. Many facets of online programs have begun to provide full-fledged quality education in the U.S. right from junior level to high level. During the pandemic, the majority of educational institutions witnessed a huge decline in academic enrollments therein affecting the revenue and cash flow. As a result, a majority of the institutions offered waivers, discounts, and other forms of offers that would help them retain the enrollments. Today, as the U.S. market is reviving, digitalization in the education sector in the U.S. offers lucrative opportunities. The U.S. Education Market is propelled by the increase in the prevalence of SMART technology, the rise in consumer income, and quality spending on education. The presence of world-class technology is one of the crucial factors in the growth of the U.S. market. The market size is projected to gain upper traction in the coming years owing to the adoption of new technologies and the increase in the importance of education in the U.S. With the shift in the consumer mindset, the education sector in the U.S. is projected to witness massive expansions in the forthcoming years.

The Canadian edtech market had total revenues of $1.7 billion in 2021, representing a compound annual growth rate (CAGR) of 11.1% between 2016 and 2021. The pre K-12 and K-12 segment was the market’s most lucrative in 2021, with total revenues of $1 billion, equivalent to 57.2% of the market’s overall value. The value of the Canadian edtech market grew by 15.3% in 2021. Expenditure in the Canadian edtech peaked in 2020, as an emergency response to the lockdown measures implemented to contain the pandemic. The market is expected to grow significantly as many companies and educational institutions have implemented some form of remote learning which will boost the market positively in the coming years. Level of expenditure in the Canadian edtech market is considered low compared to other markets. However, that is because edtech expenditure is dwarfed by the level of overall expenditure on education in Canada, which is higher than the average for developed countries. Coursera, ApplyBoard, and D2L Inc are the leading players in the Canada edtech market.

Europe

The Europe e-learning market size reached US$ 67.9 Billion in 2022 and is forecasted to reach US$ 136.9 Billion by 2028, exhibiting a growth rate (CAGR) of 15.3% during 2023-2028. The Europe e-learning market is primarily driven by the presence of well-established education infrastructure. Several renowned European universities have been offering blended learning experiences to students. As a result, the demand for personalized courses and content and customized learning tools is higher in the region. Also, due to various advantages, such as accessibility to multiple classes and interactive lectures and sessions, there has been a rise in the adoption of e-learning solutions in Europe. Although covid-19 severely impacted the region, this pushed many companies to opt for e-learning platform. Educational institutions also had to entirely shift from classroom lectures to virtual classrooms.

Germany is the European Union’s strongest economy (EU). The Germany market dominated the Europe Education Technology Market by Country in 2021 and would continue to be a dominant market till 2028; thereby, achieving a market value of $19,373.5 Million by 2028. The UK market is poised to grow at a CAGR of 14.3% during (2022 – 2028). Additionally, The France market would display a CAGR of 16.1% during (2022 – 2028).

Nigeria

Nigeria’s population is estimated to have passed 200 million people in 2019, making it the most populous country in Africa and seventh most populous in the world. The population is growing at an annual average of 2.7%, which is faster than the continental average, bringing with it pressure on the resources available for public programmes. More than half of the population is estimated to be eligible for education, and 4 in every 10 people in the country are eligible for basic and senior secondary education. In the past decade, the school age population increased by 23 million, with the government having to create structures to accommodate existing requirements, as well as the additional children and youth. The implication of not meeting this demand is the loss of the opportunity to equip children and youth with functional literacy and the skills needed for gainful employment. This demonstrates the immense pressure this sector alone exerts on public resources.

Statista

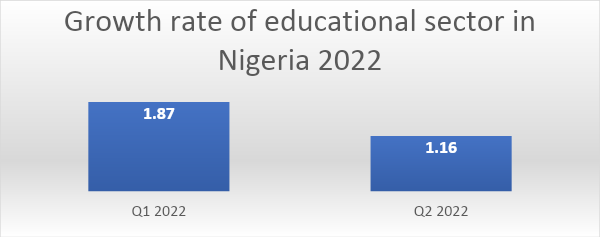

Real GDP growth of the education sector in Nigeria from first quarter to second quarter 2022

Education and training in Nigeria are offered at pre-primary, primary, junior secondary, senior secondary, technical, and vocational education and training, tertiary and higher education, and basic and literacy education. Education services at these levels are delivered at public and private institutions, and through formal and non-formal streams. In 2018, there were more than 7 million children attending pre-primary school, while Junior secondary enrolled 6.65 million students during the 2018/2019 school year, 3.17 million in rural and 3.48 million in urban schools. In senior secondary, two in three eligible children were estimated to be attending school. According to the 2018/2019 Nigeria Living Standards Survey (NLSS), the gross attendance ratio in senior secondary is estimated to have been 66%. In post-secondary, which comprises technical and vocational training, tertiary colleges, and universities, there were about 4.66 million trainees and students enrolled across the three categories. Of these, 2.34 million were at university, translating into 50% of the total enrolment. The country’s basic education is served by 1.7 million personnel, 1.45 million teaching and 211,500 non-teaching staff, the teaching staff accounting for 87% of the total personnel in schools.

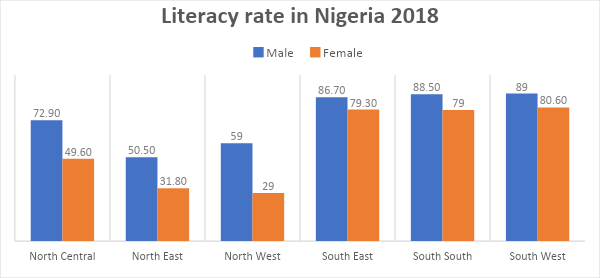

Literacy rate in Nigeria in 2018

Statista

The highest literacy rates in Nigeria were registered in the southern regions of the country. In the Southwest, 89 percent of males and 80.6 percent of females were literate as of 2018. Also, the south zones showed the lowest percentage differences between male and female literacy. Female literacy rate in Nigeria is among the highest in West Africa. The highest female literacy rates were registered in Cabo Verde and Ghana, while Nigeria ranked third.

Books are at the core of a nation’s development — economic, educational, literary, socio— cultural, political. Among other cultural values of the book, books are agents of social and cultural change and important sources of information for personal development. Thus, many nations tenaciously developed their book industries to improve their literacy rate. In Nigeria, the improvement in literacy started with the book/publishing firms. Through the production of educational materials, more people began having access to books, and the overall reading culture among people improved. Today, the advent of technology has revolutionized the way people learn. In Nigeria, technology has become an important key in the Nation’s improved literacy rate.

In 2018, the country spent a total of N1.76 trillion on education covering Early Childhood Care, Development and Education (ECCDE), primary, secondary, technical, and vocational training, and tertiary education, as well as administrative and oversight functions at the federal, state, and local governments. Eighty-five per cent of the spending was on recurrent items, while the complement was spent on development. The spending represented about 1.4% of the GDP, which is below the 4 to 6% recommended spending on education for countries pursuing quality and equitable education opportunities and lifelong education for all. The low level of spending undermines effective service delivery in the sector as it is not adequate to sustain the detailed structure described previously. For instance, salaries account for 90% of recurrent spending in the country’s education sector, leaving only 10% for operations and the acquisition of materials that support learning such as books, aids, and teaching effects.

By level of education, basic education accounted for some 44% of recurrent sector spending, with primary using 29%, and junior secondary 15%. Senior secondary accounted for a further 12%, making both secondary levels together account for 27% of sector spending. Higher education accounted for 28%, meaning that primary, secondary, and higher education consumed almost similar resources. In terms of spending per student, there is a notable lack of equity with the amount observed to be generally increasing with advancing levels of education. The government spends nearly twice as much on secondary school students in comparison to primary school learners, and seven times more on a student in higher education compared to a child in primary school. The low public spending means that households must share the costs of educating their children. Households spend about N17,000 per learner in a year, with rural families spending much lower than urban households. Similar to the structure of public funding, household contribution increases with advancing levels of education, ranging from N1,800 for learners in non-formal education to N13,400 in ECCDE, N9,400 in primary, N18,000 in junior secondary, N24,000 in senior secondary, N67,000 in Technical and Vocational Education and Training (TVET), and N86,000 in universities.

Institutions

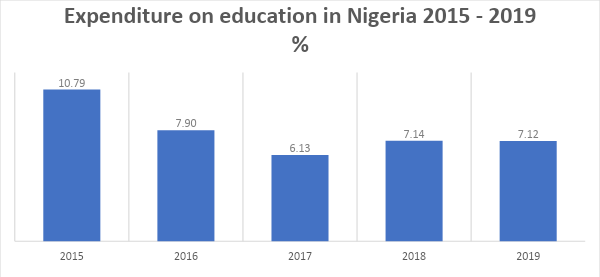

In 2019, the expenditure on education in Nigeria amounted to 7.12 percent of the total Federal budget. Between 2015 and 2019, the share of federal budget invested on education fluctuated. Overall, the highest figure was reached in 2015, when over ten percent of the national budget was allocated to the education sector.

Statista

Allocation to education sector as share of total Federal budget in Nigeria from 2015 to 2019

Public Universities

The overall goal of the Nigerian tertiary education system is to produce highly skilled individuals who will contribute immensely to the development of the nation and the global community. Because education is essential to the government, they allocate a portion of the yearly budget to educational institutions through various bodies. One such funding is the Tertiary Education Trust Fund (TETFUND). The government serves as the primary source of funds for public universities in Nigeria.

The federal government uses the Tertiary Education Trust Fund (TETFUND) to facilitate the execution of capital projects across educational institutions in the country. The funds are raised through a compulsory 2% education tax imposed on the profit of all registered companies in Nigeria. The funds generated are then used to assist in capital project commencement, completion, and rehabilitation. It also helps provide and upgrade facilities for teaching, learning, research, and developing the requisite human capital. This fund is disbursed and managed by an eleven-member board with members drawn from the six geopolitical zones of the country as well as the representative of the Federal Ministry of Education, Federal Ministry of Finance, and the Federal Inland Revenue Services.

For universities, the funds are managed through the Nigerian Universities Commission – a buffer organization that assists the government in coordinating the affairs of the universities. Although it comes from the government, there are differences in the amount released to universities. These funds are then distributed as subventions and are calculated based on the staff strength, number of students, locations, and other factors. Since it is at the government’s discretion, it is highly dependent on the year’s budget.

The 2022 top five universities with the highest allocation include,

| Universities | Capital Allocation |

| University of Ibadan | 17.1 billion |

| University of Benin | 17.8 billion |

| University of Calabar | 19.8 billion |

| Ahmadu Bello University, Zaria | 22.6 billion |

| University of Nigeria, Nsukka | 24.2 billion |

Breakdown of Allocations from sample Universities

| Universities | Capital Allocation | Personnel cost | Overhead cost | Capital Expenditure |

| University of Benin | 17.8 billion | N16.859 billion | N171.850 million | N791.989 million |

| University of Jos | 12.05 billion | N11.346 billion | N262, 164 | N544.758 million |

| Obafemi Awolowo University | 12.05 billion | N11.198 billion | N173.248 million | N633.634 million |

Private Universities

The increasing complexity of the Nigerian society because of social changes has affected the educational institution, most especially, the tertiary level of education. The Federal Government has introduced some novel practices to contend these pressures one of which is the privatization of higher education for standards and quality; increased access and better funding to meet the needs of globalization and the deregulation of hitherto publicly managed organizations. Private university education is unarguably one of the growing trends in the education system in the world. The idea of private initiative in advancing the university education in Nigeria is a popular initiative that has received accolades from citizens. Protagonists of private investors believed that the development of education should not be vested in government alone, rather; it should include the investment of individuals who wishes to contribute to the development of university education. Today, there are over 70 private universities in Nigeria, and some of the top schools include, Igbinedion University, Babcock University, Covenant University, Pan-African University, and Afe Babalola University, amongst others.

Private vs public

Funds from proprietors constituted 78% of the total funds available to universities in Nigeria. The State government owned university relies the most on their proprietors for funds (90% of total funds are from the government) this is followed by the Federal government university in which64.8% of the funds is from its proprietor whereas the private university depends the least on its proprietor and relies more on other alternative sources of funding. The cost of graduate production is the highest in the private university (US$9,168) and the lowest in the State-owned university (US$ 4,835). The low unit cost observed in the public universities could be due to the low level of funding by the government and the increase in student enrolment which was not commensurate with increase in funding. This agrees with the World Bank report in 2010 that says universities in Africa find it increasingly difficult to maintain adequate student-teacher ratio, lecture halls are overcrowded, buildings fall into disrepair, teaching equipment is not replaced, and investment in research is insufficient. This evidently shows inadequate public financing and resource diversification which at the end results in a deterioration in quality of graduate output. Since more and more sectors of the economy continually keep demanding for more and more of the scarce resources from the government, government owned institutions may continue to be underfunded. Government owned universities have relied too much on their proprietors for funding, the attendant effect being the observed lower unit cost of graduate production, an indirect indicator of production of low-quality graduates.

Leading Nigerian universities as of 2023, by position

| Position in Global Ranking | ||

| Nigeria rank 2023 | World University Ranking 2023 | University |

| =1 | 401–500 | University of Ibadan |

| =1 | 401–500 | University of Lagos |

| 3 | 601–800 | Covenant University |

| =4 | 1001–1200 | Bayero University |

| =4 | 1001–1200 | Federal University of Technology Akure |

| =6 | 1201–1500 | University of Benin |

| =6 | 1201–1500 | University of Ilorin |

| =6 | 1201–1500 | University of Nigeria Nsukka |

| =6 | 1201–1500 | Obafemi Awolowo University |

Times Higher Education

The 2023 data set shows that the University of Ibadan is the leading University in Nigeria. It was founded in 1948 and is the oldest university in the Country.

Publishing Firms

The publishing industry is evolving. We see this in the ever-changing scope and scale of economies. For example, with the advent of digital technologies, consumers are increasingly buying and reading books online, and publishers are struggling to keep up. eBooks growth rate has increased exponentially in the past ten years while the print books market declined drastically, especially in the past three years. The global book publishing industry declined from $92.8 billion in 2019 to $85.9 billion in 2020. In this era where there is a plethora of data, books are here to serve as a repository of information to guide, stimulate mental formation, and promote growth and development in societies.

Although books offer many benefits, especially in shaping societies, the powerhouse – that is, the publishing industry, that governs its production continues to suffer various setbacks. Problems such as undercapitalization, piracy, self-publishing, digital revolution, lack of infrastructure, inadequate technological know-how, and others, are many of what affect the industry. The publishing industry is one of the oldest industries in Nigeria. In 1925, the first Nigerian Printing and Publishing Company got established, and with technological innovations, the company became successful and an inspiration to emerging firms in the industry. The publishing industry was growing, and the demand was growing. With the introduction of computers in the 70s and 90s, it became easier to meet the quality requirements of print jobs. However, while publishing in Nigeria had some great levels of development, today, we see a drastic decline. Today, issues pertaining to undercapitalization, piracy, self-publishing, digital revolution, lack of infrastructure, inadequate technological know-how have contributed to the industry’s decline.

The 1978 Nigerian Enterprises Promotion Decree provided that at least 60% equity participation in book publishing must be by Nigerian nationals. With effect from that year, book publishing in Nigeria became indigenous, making it unnecessary to distinguish any longer between indigenous and foreign publishing in the country. The foreign publishing companies (notably Oxford University Press, Longman, Macmillan, Heinemann, Evans) which dominated (and still dominate) the publishing scene in Nigeria, reduced foreign equity participation to 40% or less, and some took new names (e.g., University Press Plc in place of Oxford University Press). Today, the book publishing in Nigeria is essentially a private sector affair. Because of the absence of pre-determined qualifications or conditions to be met, book publishing is one of the most unregulated industries in Nigeria. And it is grossly undercapitalized. The Federal Military Government made an unsuccessful attempt in the 1970s to set up a government publishing company. Some government agencies, State Ministries of Education, and professional associations have played an active part in developing primary and secondary school textbooks, but they have generally done so in collaboration with book publishing houses.

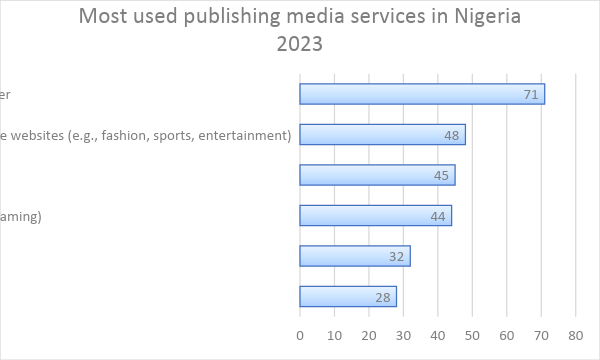

Most used publishing media services in Nigeria

Statista

EdTech

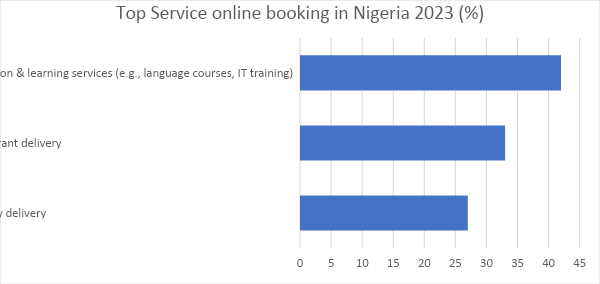

Nigeria is one of the fastest-growing tech hubs in Africa, with a thriving tech industry and a growing number of startups. The country has a large and young population, a rapidly expanding economy, and a growing demand for technology-based solutions to its many challenges. Edtech is a significant area in the tech space in Nigeria, and it is improving the educational sector in Nigeria, by bridging the gap between the number of students and the limited resources available to schools and universities. More schools are integrating EdTech into their learning environment, ranging from school information management to student attendance and the results have been promising. Schools that have adopted Edtech in their schools have reported an increase in productivity and efficiency. Recent EdTech trends in Nigeria include the use of digital learning tools and strategies to boost student performance and increase productivity and efficiency, and also for teacher training and development. Private schools are the leading pioneers of EdTech in Nigeria, especially for administrators that understand how paramount it is to yield a desirable output. Some Nigerian EdTech companies like Flexisaf Edusoft Limited have leveraged technology to make education seamless and accessible to millions of Nigerians by providing School management software solutions such as SAFSMS – a complete school management solution that drives students’ learning, enhance parents’ engagement, improve teachers productivity, and also reduce cost and efficiency. Top five education technology companies in Nigeria 2021 include uLesson, Edukoya, AltSchool Africa, Edves, and Stanerd.

Statista

Sectors in Education Industry

The education industry is divided up into four sectors, and each of the sectors caters to a growing demand for cutting-edge education products and services. Each category has distinct market segments, all of which are defined in this article. The first category is schools/ service providers. This sector produces elementary and secondary education, alternative/special education services, education management organizations, charter schools, virtual schools, and proprietary schools. The second sector, the supplemental education service providers provide higher education and vocational education. This classification also includes learning centers, tutoring services, and various assessment services. Educational products & services sector, which is the third sector, produces and supply educational material and products including educational products, publishing, and supplemental products. The last sector is the Education support services sector. This sector provides support and ancillary services to the education industry including education consultants, education information and research, education investment services, education policy specialists, and technology services.

Key Players in the Industry

There are many actors involved in the offering of a school-based personal finance curriculum. Curriculum and Instruction Specialists School districts may have individuals assigned to select/develop and implement curriculum that meets the learning objectives for the district. These individuals can assist with researching financial education curricula to determine what may work best for the district. Parent Teacher Organizations (PTO) Parent teacher organizations exist as a liaison mechanism between parents and the staff at the school. PTOs can help set weekly areas of focus and encourage participation using community-funded prizes, advertising mechanisms, special events, etc. School Administrators Schools typically have an assigned principal and may have several vice principals assisting with administrative duties. Because principals are on the front lines, interacting with parents at their schools, they are often aware of emerging issues in education. As parents bring concerns to administrators about a lack of financial education in their schools, principals may forward these concerns on to the school board and other staff with the board of education.

The local school board is usually comprised of elected officials. They are responsible for hiring the superintendent, developing policies, curriculum, and the school budget. Public meetings of the school board are held on a regular basis. State Legislators State legislators are voted in by residents. When the legislature is in session, legislators create and process bills that may become laws. Legislative committees and subcommittees focus on issues in related areas, and there are typically committees that meet to discuss issues related to education in the state. Teachers work to meet the administrative tasks they have been assigned, while also helping children develop individually. When parents have concerns about areas of growth for their children, teachers respond and try to find ways to improve the areas of concern. Teachers may also be creative in finding ways to teach areas of interest, such as personal finance, using their elective areas or time in teaching. Publishing/book firms who manufacture educational materials are also key players in the industry. Other players include service providers like the technological companies.

Entering the Education Industry

The education industry is a vast and varied one, playing a significant role in countries around the world. From pre-school through to universities, there is a wide range of institutions and organisations that are directly involved in learning. In addition, there are governmental and policy roles, eLearning organisations, technology companies, publishing firms, educational bodies, and much more. As we see, the roles across some of these sectors varies. Although teachers play a central role, they’re far from the only profession. Support, admin, development, policy, finance, and other areas are also vital to the education industry. Because of how vast and varied it is, there are several routes into the numerous sectors. However, for all roles or sectors, the basics is getting adequate education, training, and experience.

Students

Nigeria follows the 6+3+3 system of primary-secondary education. Six years of primary education are followed by three years of junior secondary education and three years of senior secondary education. Elementary education in Nigeria is six years in duration and runs from grade one through six (ages 6-12). Students are awarded the Primary School Leaving Certificate on completion of Grade 6, based on continuous assessment. Junior Secondary Education is 3 years (ages 13-16) Grades 7-9. Students are awarded the Basic Education Certificate (BEC) on completion of Grade 9. Students must achieve passes in six subjects, including English and mathematics, to pass the Basic Education Certificate Examination. Senior Secondary Education is 3 years (ages 16-19) Grades 10-12. Upon completion of Grade 12 in May/June, students sit for the Senior School Certificate Examination (SSCE). They are examined in a minimum of seven and a maximum of nine subjects, including Mathematics and English, which are compulsory. Successful candidates are awarded the Senior Secondary Certificate (SSC). Most universities require passes in at least five SSC subjects and an average grade of at least ‘credit’ level (C6) or better to be considered for admission. SSC examinations are offered by the West African Examination Council and the National Examination Council (NECO). The Federal Ministry of Education is responsible for overall policy formation and quality control. Secondary School education is largely the responsibility of state governments and Elementary School education the responsibility of local governments.

Institutions

Primary, Secondary, and Universities

Basically, schools controlled and run by the federal government have no required license to operate, except for request for approval from state government to the federal education board. However, for private schools, there are requirements to be possess. For instance, in Nigeria, the school should have a qualified and certified staff, must have registered at the Corporate Affairs Commission (CAC), should have standard required infrastructure and social amenities, and relevant approvals from the Ministry of Education. The National Universities Commission (NUC) is a government commission for promoting quality higher education in Nigeria. The Parastatal functions by granting approval for all academic programs run in Nigerian universities and by ensuring their quality assurance. For a private university, an interested applicant is expected to apply in writing, to the Executive Secretary, NUC, stating the intent for the establishment of the university. The declaration of intent should include, in brief, the name of the proposed University, the location, the mission and vision, the nature of the proposed university and its proposed focal niche in the current Nigerian University System, etc. The Federal Executive Council considers the recommendations of the NUC Board and Security report on the proposed university’s Promoters. If approved, a three-year Provisional License is granted the applicant. Only satisfactory performance during the probationary period will earn the applicant a substantive License.

Companies (Publishing firms, Technological firms, other Education providers)

The education market is highly competitive; to survive in the competitive environment, businesses must do their due diligence. As the industry and technology develop, so will the opportunities to enter more market boundaries. An efficient way of achieving this is through quality education market research. An abundance of programs and courses that are more widely available (i.e., remotely offered) means more students have more options. These companies supplying them, must then distinguish themselves if they want to attract and sustain the attention they need for success. Education market research helps reveal the current market landscape, including an overview of existing and potential competitors, industry trends and the most effective positioning strategies. Approvals and Licenses are also very important requirements in accessing the industry. In Nigeria, the Nigerian Publishers’ Association (NPA) is the statutory body that governs the activities of publishing firms. Alongside the NPA, Nigeria has the following major professional associations in the book sector: Association of Nigerian Authors, Nigerian Booksellers Association, Association of Nigerian Printers, and Nigerian Library Association. Authors have additional writers’ associations including the Academic & Nonfiction Authors Association of Nigeria, the Association of West African Young Writers), and Women Writers in Nigeria. The Nigerian Communications Commission (NCC) is the independent regulatory authority for the telecommunications industry in Nigeria. Depending on specific services an Edtech company intends to engage, a registered Edtech company is also required to obtain a Telecommunication License from the NCC.

Workers

There are many categories of workers in the education industry. While some workers are required to have direct contact with learns some don’t, but only have supporting roles in the industry. The first category is that of the teaching roles. These workers usually have a more hands-on types of roles. They are required to have direct contact with learners, often planning out materials and learning plans. These workers include the teachers, lecturer, and private instructors. Basically, to fit into the role. These workers need to have high level of skills and knowledge in their field, other times, BSc, Masters, and Ph.D. degree certifications, but most importantly a license to practice. The other category is the educational support roles. These roles often support the work of other education professionals, as well as the learners themselves. They’re not quite as hands-on as teaching roles but do sometimes have some level of direct interaction. They include the educational psychologist, teaching lab technicians, and the librarians, amongst others.

Entry Outline

Education – Whether a worker decides to go into the teaching, supportive or administrative role, education continuously plays a central role. To become a qualified worker, you’ll need to qualify as one first, which usually requires a relevant degree/certification. In Nigeria, the least qualification for a teacher is a N.C.E qualification.

Training – Some roles in the education industry can be attained through relevant training. Internships, apprenticeships, and other similar courses can help one learn and gain experience in your chosen field.

Experience – For some roles, you can start at an assistant level and work your way up as you gain experience and work-based learning.

License – Licenses are similar to certifications, as they indicate competency of a set of standards and must be renewed with continuing education. However, unlike certifications, licenses are mandatory to legally practice an occupation. All states in various regions require that people be certified before they can teach in schools. The rigorous process for licensing ensures that teachers meet certain standards in their subject areas, pass required background checks for the age groups they teach, and are up to speed in accepted teaching methods. To apply for registering as a Teacher in Nigeria, the applicant must first take a Professional Qualifying Examination (PQE) conducted by the Teachers Registration Council of Nigeria. For that, the applicant has to visit the State office of Teachers Registration Council of Nigeria. The PQE is a license to teach in Nigeria; upon successful completion, a teacher is required to renew the license every three (3) years.

PESTLE Analysis

Political Factors

The education industry is highly sensitive to political changes, and decisions made by governments can have long-lasting effects on the quality, accessibility, and direction of education within a country or region. Stakeholders in the education sector, including institutions, educators, students, and parents, closely monitor political developments to anticipate potential impacts on their educational landscape. For instance, education, as we know is a significant part of a country’s public expenditure. Governments allocate budgets for education, which impact the resources available to educational institutions and the quality of education they can provide. Changes in funding levels can influence infrastructure development, teacher salaries, and the availability of educational resources. Suppose any government allocates more of the total budget to the education sector, in that case, the education industry in that country will flourish since new universities and schools will be made. On the contrary, less budget allocation towards the education sector would hinder the growth of the education industry in that country. For instance, many institutions in Nigeria, have expressed concern about the inadequacy of government funding. They have expressed that this insufficiency has contributed to the resulting months of strikes and disruption in the educational system university management. Thus, after reviewing its funding to federal institutions, the Federal Government has compelled administrators to start generating at least 10 percent of their total revenue. This directive has led institutions to find innovative ways to generate funds internally from their available resources.

Besides that, the government’s tax policies impact the education industry significantly. More private educational institutions will be made in a tax regime that provides tax incentives to educational institutions. As a result, the education industry will grow. On the other hand, if the education sector is slapped with high taxes, many educational institutions might close down, giving the education industry a major setback. Political stability also plays a major role; a politically stable environment will encourage people to attain education. Political decisions can also impact the adoption and integration of technology in education. Governments may invest in edtech initiatives or create policies that promote digital learning.

Economic Factors

Various economic factors significantly affect different industries, similarly, factors related to the country’s economy also impact the education industry. The availability of financial resources for educational institutions affects their ability to provide quality education and invest in infrastructure, technology, and faculty development. The cost of education, including tuition fees, textbooks, and other expenses, influences access to education. Affordability can affect enrollment rates and the type of educational institutions students choose. For instance, private educational institutes have a significant percentage in the entire education industry; however, private education is always expensive. Hence, people require a lot of money to attain the education.